The cannabis industry is a complex and ever-changing landscape, which presents unique challenges for businesses operating within it. Managing risk is critical for the success and sustainability of any business. From regulations to supply chain issues, it’s essential to understand the potential risks associated with the cannabis industry and develop comprehensive strategies to mitigate them.

Managing risk is very important for businesses that work with cannabis because they must follow many rules and regulations. It is also important to make sure the supply chain works, which means getting things from one place to another without any problems. Understanding risks and making plans so these problems don’t happen can help your marijuana business stay successful. Benjamin Franklin once said, “an ounce of prevention is worth a pound of cure.” When it comes to managing risk, this statement is profoundly true because a bit of planning will help you avoid extremely costly mistakes.

Step One: How to Identify Risks in your Marijuana Business

One of the most important steps in managing risk is to identify the risks that could potentially affect your business. To do this, it’s important to consider all aspects of your enterprise and ask yourself which areas are more vulnerable. It is also a good idea to consult with experts in the industry who can offer valuable insight into potential risks you may not have considered.

Common Risks Faced by Businesses in the Marijuana Industry

- Regulatory Risk

- Supply Chain Risk

- Financial Risk

- Reputational Risk

- Legal Risks

- Operational Risks

- Market and Pricing Risks

When identifying risks, it’s crucial you write things down so you can review and adjust your risk management plan as needed. Start by looking back at past incidents and identifying potential risks for your company. Examining trends in customer complaints or insurance claims can provide insight into areas where there may be greater potential for threats to arise. Next, ask yourself the “what ifs” questions. What if our payment processing account stops working? What if this law is passed? As you think through possible scenarios, write them down as potential risks to your business. You can’t begin assessing risks until you’ve created a list of potential risks. Once your potential risks list is complete, you’re ready to begin assessing each of them.

It is important to identify potential risks early on so that you can plan ahead and be prepared if something bad happens. This way, you can do things like get insurance in case of an accident or review laws and regulations to make sure your business follows them. You might even want to set up a newsfeed on Google News to ensure you stay in the know regarding laws and regulations as they frequently change. Planning ahead will help keep your business safe and successful.

Step Two: Assessing Risks to Your Business

To assess the likelihood and potential impact of each identified risk, you should think about how likely it is that a problem will occur, and how big of an effect it could have on your business. For example, if there is a law or regulation change in the marijuana industry, you can look at how likely this change is to happen and what kind of impact it could have on your business. You can also look at past incidents to see what kind of problems occurred before and how much they cost your business. Finally, you can review your insurance coverage to make sure it covers any potential risks that may arise.

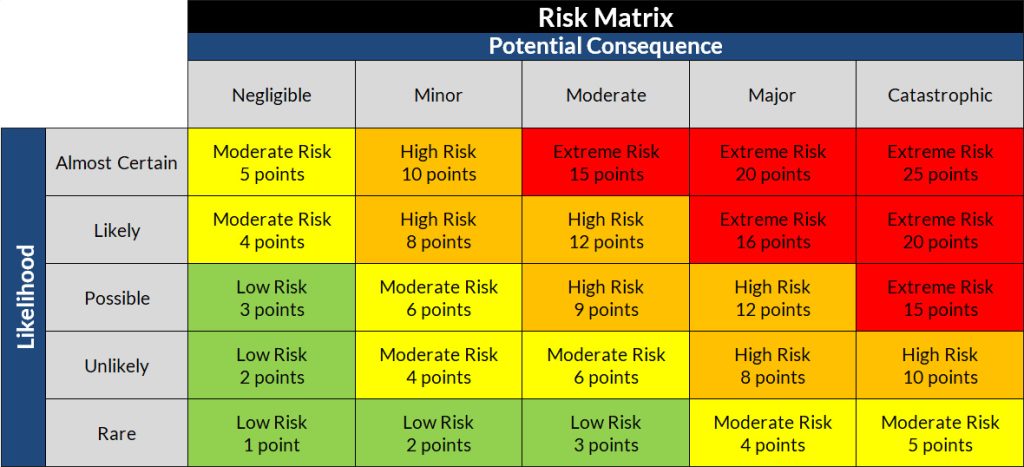

Tips for Assessing Risks

One of the best ways to assess risks is to create a risk matrix. A risk matrix is a visual representation of the potential risks your business may face including their likelihood and impact on operations. The matrix will help you identify which risks are most important, so you can focus your resources on managing them. You can also use the matrix to track risk management progress and review mitigation strategies.

Download Our FREE Risk Assessment Worksheet & Risk Matrix

After downloading our free risk assessment worksheet, which includes a risk matrix, you’ll be on your way to developing a plan for how to best mitigate risks to your marijuana business. Keep the worksheet handy and review it frequently.

TIP: You may even want to print this article out to make it easier to remember the things to think about when you review and update your risk mitigation plan.

Step Three: Develop a Plan for Managing Risks

There are several strategies that can be implemented to manage the identified risks. First, for physical security risks such as theft or natural disasters, installing security systems with motion sensors, cameras, and alarms can help deter potential intruders. Additionally, implementing strict cash-handling procedures such as using automated POS systems, conducting regular audits, and requiring two-factor authentication for online transactions can help protect your business from internal and external fraud. Physical security risks can also come from employees. Be sure to conduct background checks on all employees and provide training to employees that will aid in mitigating risks to your business, such as how to protect sensitive data, security policies, etc.

Conducting regular risk assessments and reviews of laws and regulations also helps to protect your business. Setting up alerts to notify you whenever there is a change in law or regulation that might impact your company can make sure you stay on top of the latest changes. Having adequate insurance coverage is also a good way to protect your business from potential legal liabilities and financial losses due to unexpected events. Regularly reviewing your policy can help make sure it covers all the risks associated with running a marijuana business.

Conducting regular risk assessments and reviews of laws and regulations also helps to protect your business. Setting up alerts to notify you whenever there is a change in law or regulation that might impact your company can make sure you stay on top of the latest changes. Having adequate insurance coverage is also a good way to protect your business from potential legal liabilities and financial losses due to unexpected events. Regularly reviewing your policy can help make sure it covers all the risks associated with running a marijuana business.

Finally, outsourcing certain tasks such as bookkeeping, web development, advertising & marketing, and financial management can help manage risks by ensuring that you have a reliable source of expertise to call upon should any issues arise. It’s crucial that you select third-party service providers who specialize in serving the marijuana industry so that they are familiar with, follow, and stay up-to-date on the frequently changing laws and regulations. For example, there are very few merchant account providers that specialize in the marijuana industry. As of the time of this article’s writing, Visa, MasterCard, Amex, & Discover do not allow credit cards to be used for the purchase of marijuana products. However, debit cards that bear the same credit card issuer logos can be accepted as a payment method for purchases of marijuana and marijuana products.

One example of a fully compliant and totally legal debit card payment processor is Unity Payments. Their worry-free solution makes it easy for customers to pay online or in-store using a debit card. New customers even receive their first payment terminal for free. While Unity Payments allows their clients to accept debit cards in a legal manner, there are many shady companies promoting fraudulent Cashless ATMs that attempt to circumnavigate the legal system by pretending to be an ATM that someone is withdrawing cash from, when in fact transactions are being done to purchase marijuana and marijuana products. Just remember, when selecting a third-party service, you are in control and are responsible to make wise decisions to ensure the companies you do business with do so in a manner that is compliant and abides by all current laws.

In Conclusion

In conclusion, managing risks associated with running a marijuana business is essential in order to ensure success and avoid legal liabilities. Proper physical security measures such as installing alarms and cameras, employee training and background checks, risk assessments and reviews of laws & regulations, adequate insurance coverage, and outsourcing certain tasks can help protect your business. Careful consideration should be taken when selecting third-party service providers to do business with in order to ensure compliance with all current laws. By taking these measures you can minimize risk and ensure your business remains compliant with all applicable laws.

0 Comments